UK State Pension payment dates usually follow a 4-week cycle rather than a fixed calendar date. This means most people receive 13 four-week payments across 52 weeks, while household bills may still leave on monthly dates. This guide explains payment weekdays, first payments, bank holidays, tax and a practical way to convert weekly pension income into a monthly budget.

How Do UK State Pension Payment Dates Work?

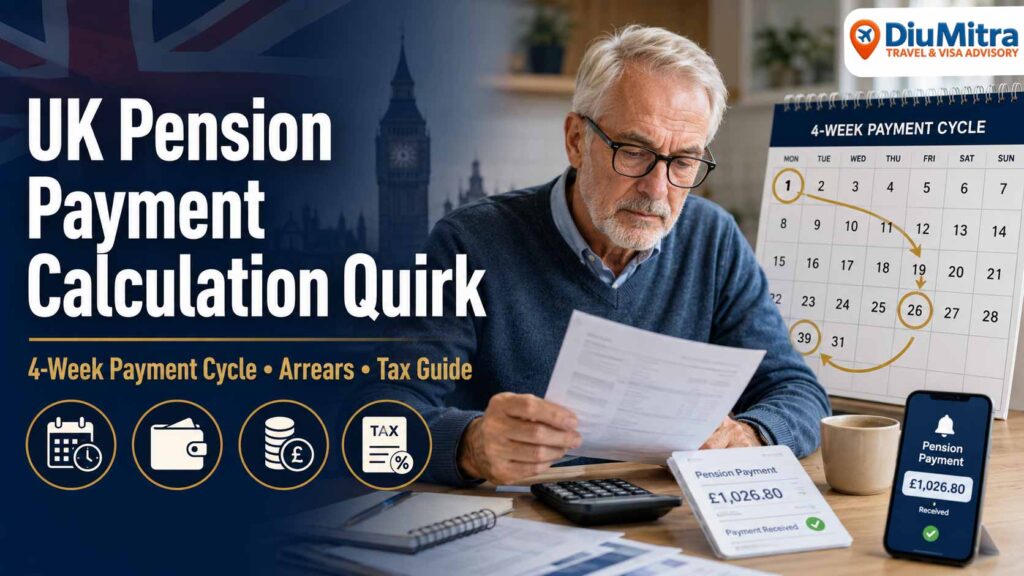

The new State Pension is usually paid every four weeks. Your normal weekday depends on the final two digits of your National Insurance number. Thirteen four-week payments cover 52 weeks, so the thirteenth payment is not a bonus. For 2026/27, the full new State Pension is £241.30 a week.

Checked 21 July 2026: figures and payment rules were reviewed against current GOV.UK guidance. Your award letter and personal State Pension record determine what you actually receive.

Understanding the four-week State Pension cycle makes it easier to plan monthly bills and recognise when a payment needs checking.

Why Is the State Pension Paid Every Four Weeks?

GOV.UK says the new State Pension is usually paid into your account every four weeks. A four-week payment covers 28 days, while a calendar month can contain 28, 29, 30 or 31 days. Your bank deposit therefore does not stay on the same date of each month.

The important distinction is between payment frequency and annual entitlement. Thirteen four-week periods equal 52 weeks. Receiving 13 deposits does not mean DWP has paid an additional month or an extra four weeks of pension.

Each deposit normally covers four weeks. The cycle moves through calendar months because it is based on 28-day intervals.

Rent, utilities, council tax and subscriptions may leave on fixed monthly dates, creating a timing mismatch rather than an income shortfall.

The thirteenth payment is not a bonus. It is one of the 13 normal four-week payments needed to cover a 52-week year.

UK State Pension Rates and Budgeting Figures for 2026/27

The full new State Pension is £241.30 a week for the 2026/27 tax year. The full basic State Pension is £184.90 a week. Not everyone receives the full rate: your actual amount depends on your National Insurance record and, in some cases, protected payments or older State Pension rules.

| 2026/27 figure | Full new State Pension | Full basic State Pension |

|---|---|---|

| Weekly rate | £241.30 | £184.90 |

| Typical four-week payment | £965.20 | £739.60 |

| Annual amount over 52 weeks | £12,547.60 | £9,614.80 |

| Monthly budgeting average | About £1,045.63 | About £801.23 |

Use your own weekly award amount for planning. The most reliable personal figure is shown in your State Pension award letter or online record. People who have not yet claimed can use the official State Pension forecast service.

Which Day Will Your State Pension Be Paid?

Your normal payment weekday depends on the final two digits of your National Insurance number. Use only the digits at the end, not the final letter.

| Last two NI number digits | Normal payment weekday |

|---|---|

| 00 to 19 | Monday |

| 20 to 39 | Tuesday |

| 40 to 59 | Wednesday |

| 60 to 79 | Thursday |

| 80 to 99 | Friday |

For example, a National Insurance number ending in 48 normally corresponds to Wednesday. Once you know the weekday and one confirmed payment date, count forward in four-week intervals to create a planning calendar.

When Will Your First State Pension Payment Arrive?

Your first payment is not automatically made on your State Pension age birthday. When you claim, you choose when you want payments to start. GOV.UK says the first new State Pension payment will be no later than five weeks after that chosen date.

You will then normally receive a full payment every four weeks. You might receive part of a payment before the first full payment, but this is not guaranteed for every claimant. The DWP letter confirming your payment schedule tells you the dates and amounts to expect.

What Happens When the Payment Day Is a Bank Holiday?

You might be paid earlier when your normal State Pension payment day is a bank holiday. The exact arrangements are normally confirmed through official DWP information, and the earlier deposit does not increase your pension entitlement.

Treat an early bank-holiday payment as money for the same four-week period, not spare cash. The next payment will usually return to the normal schedule, so the money may need to last longer from the date it reached your account.

Why Can the First Payment After the April Increase Look Different?

State Pension rates normally increase each April. Because payments are made in arrears, the first deposit after an uprating date can cover days at the previous rate and days at the new rate. It may therefore be lower than a complete four-week payment calculated entirely at the new rate.

This does not necessarily mean the increase has been missed. Check the period covered by the payment and allow for the transition between rates. A later four-week payment covering only days after the uprating should reflect the new weekly amount, subject to your personal entitlement.

Is the UK State Pension Taxable in 2026/27?

Yes. State Pension is taxable income, but DWP does not deduct Income Tax before paying it. You only pay tax when your total taxable income is higher than your available personal allowances.

The standard Personal Allowance for 2026/27 is £12,570. The full new State Pension annual rate is £12,547.60, leaving £22.40 below that standard allowance. Your own position may differ because you may receive less or more than the full new rate, have a different allowance, live in Scotland, or receive other taxable income.

The four-week payment pattern does not create extra taxable pension income. HMRC normally works with the taxable annual State Pension amount, not the number of bank deposits appearing in a calendar month.

How HMRC May Collect Tax

- Through another PAYE income: HMRC may adjust the tax code used by an employer or private pension provider.

- Through Simple Assessment: HMRC may send a bill when tax cannot be collected automatically, including where State Pension is the only income and tax is due.

- Through Self Assessment: This may apply when your wider tax circumstances require a return.

Check your personal tax account or contact HMRC when a tax code or bill does not match your income. DiuMitra provides general guidance only and does not provide regulated tax or financial advice.

How to Budget a Four-Week Pension Against Monthly Bills

A useful planning method is to convert the weekly entitlement into an annual amount and divide it by 12. This gives a monthly budgeting average even though DWP continues to pay every four weeks.

Weekly pension × 52 ÷ 12At the full new State Pension rate, the calculation is £241.30 × 52 ÷ 12 = approximately £1,045.63 a month. This is an average for budgeting, not a promise that £1,045.63 will enter your account each month.

Use your DWP letter or online record rather than assuming you receive the published full rate.

Record payment dates for housing, council tax, energy, insurance, credit and subscriptions.

You might keep pension deposits in one account and transfer a consistent monthly amount for bills.

Do not treat a two-payment month or an early bank-holiday deposit as additional annual income.

Before setting a fixed transfer, allow for other income, irregular expenses and a reasonable buffer. The DiuMitra retirement calculator can help you compare expected retirement income and spending, but its results are estimates rather than personalised financial advice.

What Should You Do If a State Pension Payment Looks Wrong?

- Read the DWP payment letter: confirm the start date, payment frequency, expected amount and bank account.

- Check the dates covered: a first payment, bank-holiday payment or April uprating period may look different.

- Compare with your bank statement: note the payment reference, date and amount before contacting DWP.

- Check your personal entitlement: the full published rate does not apply automatically to everyone.

- Contact the Pension Service: use official GOV.UK contact details when a payment is missing, late or inconsistent with your letter.

Never publish or send your full National Insurance number through social media or an unverified messaging account. DWP and HMRC have official contact routes for personal pension and tax enquiries.

How Does Deferring the New State Pension Affect Payments?

If you reach State Pension age on or after 6 April 2016 and delay claiming, your eventual regular payment can increase. GOV.UK states that every nine weeks of deferral adds 1%, provided the qualifying rules are met. This is just under 5.8% for a full 52 weeks.

At the full 2026/27 new State Pension rate, a year of qualifying deferral would add about £13.95 a week. Deferral is not automatically suitable for everyone because it can affect tax, benefits, cash flow and how long it takes to recover the pension not received during the delay.

Review the official deferral rules and consider regulated financial advice when the decision could materially affect your retirement income.

Official UK Sources to Check

Use These for Personal and Current Information

Frequently Asked Questions

Need Help Understanding a Pension or Benefit Letter?

DiuMitra can help you read general wording, organise the questions you need to ask and find the relevant official source. We do not calculate entitlement, provide regulated financial advice or act for you with DWP or HMRC.

⚠️ Disclaimer: This guide provides general information and community signposting only. DiuMitra is not DWP, HMRC, a regulated financial adviser or a legal representative. Pension, tax and benefit outcomes depend on individual circumstances. Check current official guidance and seek qualified advice where appropriate.